Knowledge Organiser

1.4.1 How resources are allocated in a free market economy

- What is a market economy?

- What is a planned (command) economy?

- What is a mixed economy?

- What do consumers and firms seek to maximise? (2 answers)

- Price Functions: Explain the Rationing Function of price.

- Price Functions: Explain the Signalling Function of price.

- Price Functions: Explain the Incentive Function of price.

- Define Derived Demand

- Give an example of two products that are in joint supply.

- Define Joint supply

- Give an example of two products that are in joint supply.

- Define Composite Demand

- Give an example of two products that are in composite demand.

- List the assumptions that traditional economic theory gives to 'Homo Economicus', or 'Economic Person.'

- Critique of Rationality: Explain the main points of Prospect Theory

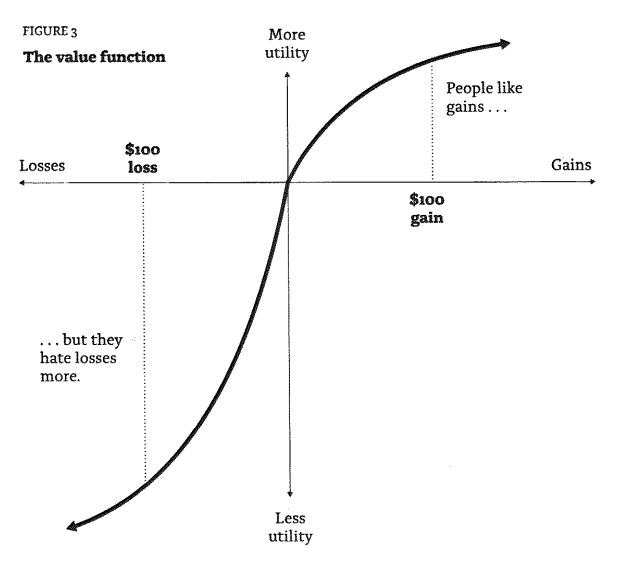

- Critique of Rationality: Sketch the Prospect Theory diagram.

- Critique of Rationality: Explain the Endowment Effect and give an example of how it is demonstrated.

An economic system that uses the market mechanism to allocate resources in society.

A system where a government, through a planning process, allocates resources in society.

A system where both free market mechanism and government planning process allocate resources in society.

Consumers seek to maximise utility. Firms seek to maximise profits.

Increases in price limit the quantity demanded by buyers in a market. The resource is rationed to those who desire it most.

Changes in price give information to buyers and sellers which influence their decisions about what they purchase and what they produce.

Changes to the price encourage sellers to produce more of the product.

When demand for a product that is based on demand for another product.

examples: -Demand for econ teachers derived from demand for econ courses. -Demand for software engineers derived from demand for apps

When one factor of production simultaneously produces two or more products from the same process.

examples: -Beef and Leather -Wool and Sheepskin -Fertilizer and CO2 -Honey and Beeswax

When a good has more than one use, so an increase in demand for one good that uses it decreases the supply of other goods that use it.

examples: -Bricks: for houses and factories -Land: for housing or offices

'The agent of economic theory is rational, selfish, and their tastes do not change' Assumes: → People have rational preferences among outcomes that can be identified and associated with a value. → Individuals maximize utility (as consumers) and firms maximize profit (as producers). with a value. → People act independently on the basis of full and relevant information.

→ Our overall level of wealth doesn't determine utility: it depends on whether we've reached it via a gain or a loss. → People feel good from gaining but they feel bad from losing twice as much. → This means that the same person can express different preferences for the same outcomes: i.e. they can be risk-averse in terms of gains but risk-loving in terms of avoiding loss.

People value items which they already own more than the same item if they did not own it. Demonstrated by: people not willing to sell a good they have at a certain price, but also not willing to purchase that good at the same price.